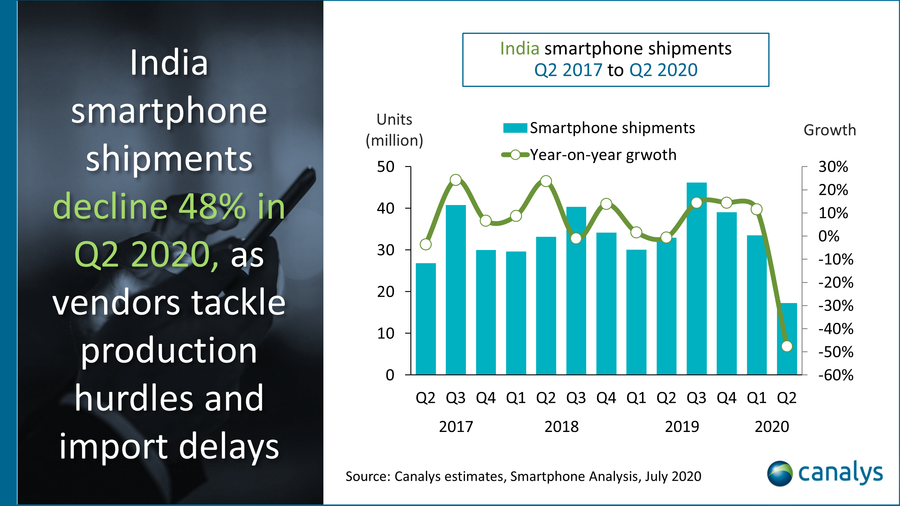

The Indian smartphone market shrank by 48% in 2020's second quarter

The Indian smartphone market in 1Q2020 appeared to experience relatively little impact from the Covid-19 lockdowns, growing by 11.5% year-on-year (YoY). This was in accordance with Canalys' research on this subject. Now, however, it is time for the results from the same firm on the next quarter on, and the situation has exhibited a complete turn-around.

This same market has fallen by a total of 48% YoY, based on the volume of smartphone shipments. The change is thought not to be related to the effects of the global pandemic (in fact, some OEMs reportedly resorted to importing units in from other regions in order to try and keep up with demand), but is instead attributed to supply issues due to the current border conflict between the country in question and China.

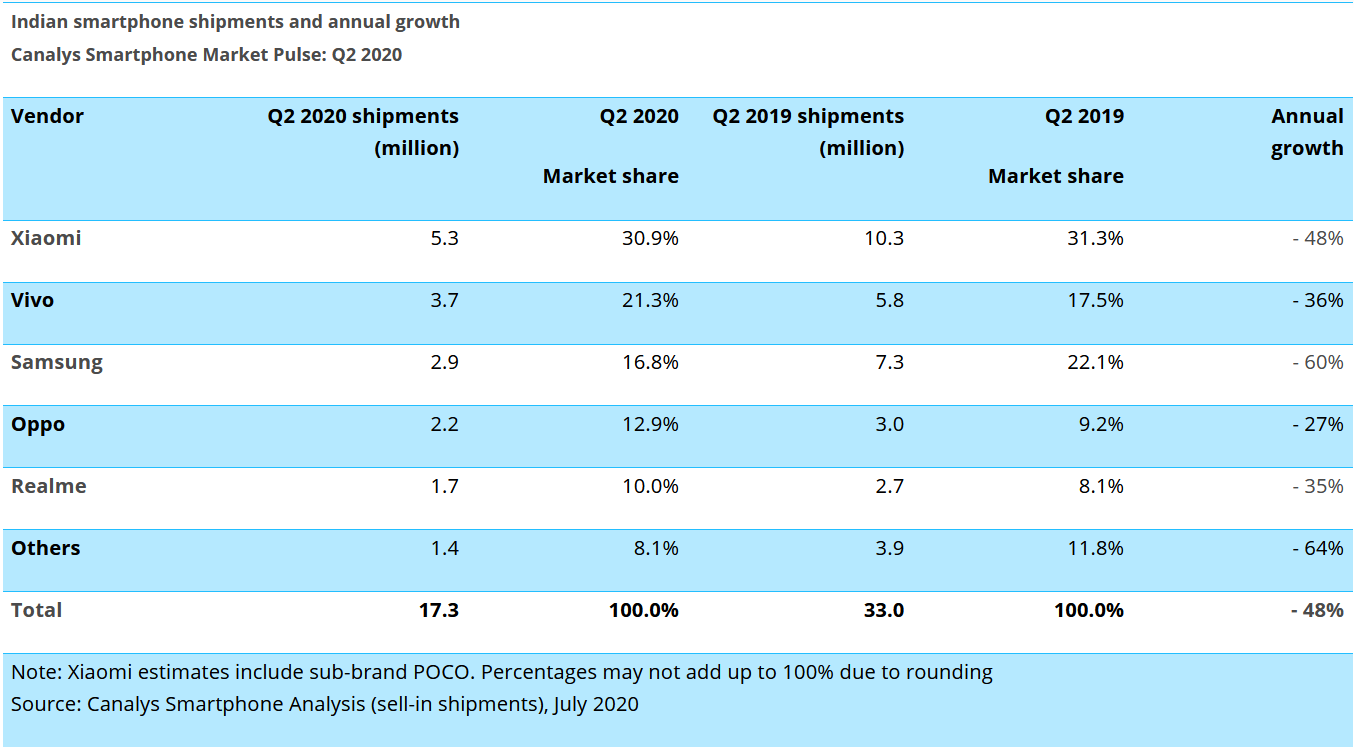

This meant that, while OEMs with manufacturing facilities in India were better off in 2Q2020, others were faced with severe supply issues. This may be part of the reason why Xiaomi/POCO and Vivo retained their top-flight places in the Indian smartphone sale charts, whereas Realme saw a partial reversal of its earlier good fortune.

This company slipped back into fifth place in terms of shipments, whereas its former fourth place was taken by its very own BBK Electronics sibling OPPO. Then again, this OEM still saw a 27% drop in its own shipments.

In fact, every top smartphone-maker posted a similar YoY shortfall, the least severe of which was that of Apple at -20%. However, Canalys does not see the Cupertino giant capitalizing hugely on this relative win in the short term due to the "hardly price-competitive" nature of its products.

Source(s)