Why does Seiko keep winning?

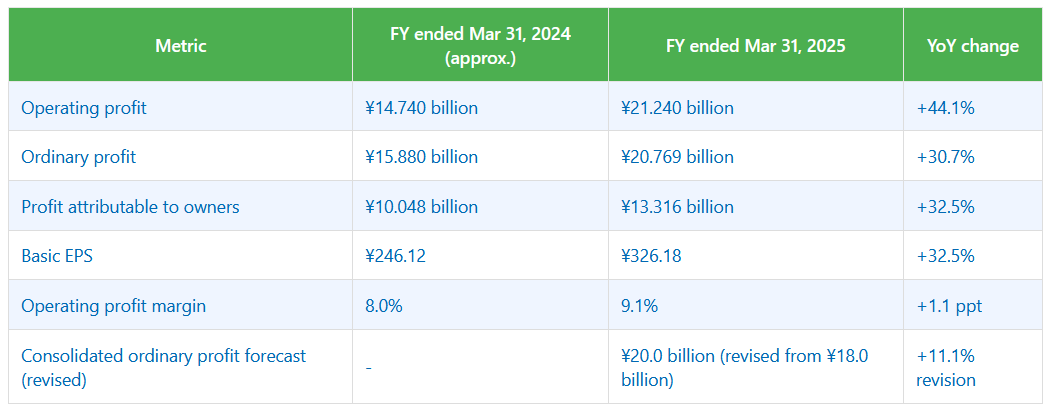

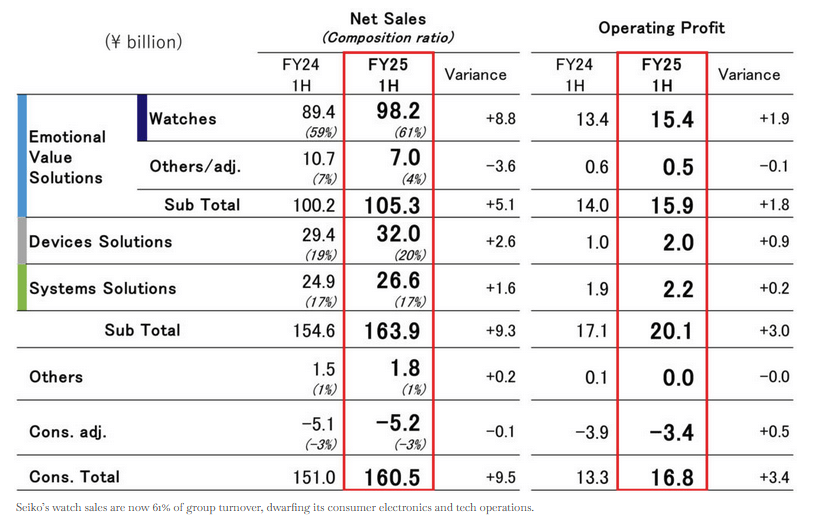

Seiko’s resurgence is no accident. In FY2025 (March-ended year), Seiko Holdings reported ¥304.7 billion in revenue - a 10.1% jump year-over-year. The drivers? Its watch business (including Seiko, Grand Seiko, Credor, Presage, Prospex, Seiko 5 Sports, etc.) is booming, and it is further fueled by solid domestic demand and a tourism rebound. In H1 2025, Seiko’s watch sales alone hit ¥98.2bn (up 8.8%) and now make up 61% of group sales. The rest of Seiko’s divisions (electronics, devices) contributed too, but the lion’s share of growth is undoubtedly in timepieces.

This growth is extremely profitable. Seiko’s watch arm runs at about a 15% operating margin, far above industry peers. (By comparison, Richemont’s luxury brands saw ~3% in H1 2026, and Swatch Group ~4.5% in FY25.) Overall operating profit jumped 44% to ¥21.24 billion in FY2025. Healthy profit translates into confidence: Seiko raised its full-year 2026 sales forecast to ¥312.0bn, and bumped up its dividend (now ¥95/share). The Japanese watch giant keeps sending a clear message to investors: Seiko’s core business is scaling up, not just selling more, but also squeezing costs and building margin.

Seiko’s strength lies in its breadth, its coverage. It spans across every watch segment - you'll find sports and diving models to everyday pieces and ultra-luxury timepieces. The company’s own insights show that new releases in Prospex (sports/diver), Presage (dress/mechanical), and Seiko 5 Sports (entry-level automatics) helped boost sales. Its high-end division, Grand Seiko, continues to become more and more popular worldwide: sales in the U.S. are strong (helped by a rising stock market), even as European luxury demand is cooling down.

Meanwhile, Seiko is working on bringing its ultra-luxury Credor brand to the rest of the world - Credor will debut at Watches & Wonders Geneva 2026 to basically follow in Grand Seiko’s footsteps. Once that happens, a Seiko watch will exist for almost every buyer and price point, which will give the company even more resilience against market swings. We can already see the results right now: Seiko is outselling many Swiss rivals; for example, one analysis states that Seiko-Epson’s annual sales exceed those of Omega and Longines combined, and Seiko’s watch sales itself are way higher than its electronics and tech divisions.

Seiko’s winning streak wasn't just born out of thin air. The corporation pioneered major watch technologies that still define the industry. In 1969, Seiko introduced the Astron, the world’s first quartz wristwatch, with a ±5 seconds/month accuracy. It later invented hybrid movements (Kinetic) and the Spring Drive (1999) - an exceptional mechanism that combines quartz timing with a mechanical power train. This legacy of R&D is one of the primary reasons for Seiko’s current appeal: it can build in-house movements and electronics across its lines, from basic quartz (as in Seiko 5) to ultra-fine Grand Seiko calibers. Plus, Seiko makes tens of millions of movements annually, giving it economies of scale few competitors can hope to match. Its in-house vertical integration (Seiko’s parent is now Seiko Epson) keeps costs lower and quality high. Also, the "Seiko mod culture" is still going strong - the company's NH35 and other movements are regularly purchased by enthusiasts off third-party websites like Alibaba for custom watches.

It won't be outlandish to say that Seiko’s gains come partly from shaking up traditional dynamics. Globally, the watch market has long been dominated by Swiss giants (Rolex, Omega, TAG Heuer, etc.). But Seiko is one of the few non-Swiss players to show rapid growth, and that too, sustainably. WatchPro reports that Seiko’s watch sales were rising faster than Richemont’s or Swatch’s, and vastly more profitable. The rise of smartwatches also hurt some Swiss stalwarts, but Seiko’s diverse portfolio and established brand in Asia buffer that pretty well. In Japan, Seiko gets the additional benefit of national pride and a growing domestic luxury segment; in China and other markets, customers love Seiko’s value-for-money stance, especially those who are trading up from basic watches. Its margins are as high as 15% in watches, which goes on to show that it isn’t just selling more - the way it is pricing its products is perfect as well.

Several recent milestones are a testament to Seiko’s strategy so far:

- Quartz revolution (1969): Seiko’s first Astron quartz watch pretty much shattered accuracy standards.

- Grand Seiko going big (2010s): Once Japan-only, it is now a world-class luxury brand.

- Seiko 5 rebranding (2020s): Upgrading its truly iconic mass-market line (Seiko 5 Sports) with modern designs and specs.

- More expansions: Building its Seiko Presage Spring Drive movements that do a great job of rivalling Swiss chronometry.

As we talked earlier, Seiko’s ongoing momentum isn’t limited to Asia alone. Grand Seiko’s in the U.S. is paying off, and new markets are opening. The upcoming (first) global showcase of Credor and the non-stop investment in marketing (especially in the U.S.) suggests Seiko isn’t really resting or taking a break. The company keeps winning again and again by balancing scale, innovation and diversification - a formula that has it competing toe-to-toe with the Swiss heavyweights.

Source(s)