AMD details much stronger financial position at their 2020 Financial Analyst Day

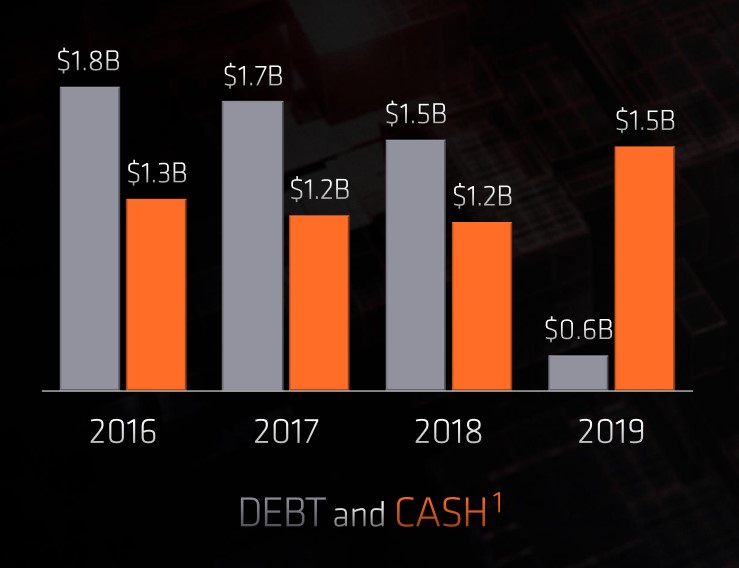

Revenue between 2016 (pre-Ryzen) and 2019 increased from US$4.3 billion to US$6.7 billion, and operating margin followed suit by increasing from 1% to 12% over the same time frame (31% to 43% gross). Perhaps the most telling sign of improvement is the change in cash and debt levels. AMD moved from US$1.3 billion cash and US$1.8 billion debt in 2016 to US$1.5 billion cash and US$600 million debt in 2019, with almost all that improvement happening during 2019.

While it would be easy to take a PC-enthusiasts perspective and assume that consumer parts have driven this growth, the most substantial growth area has been with datacentre products, and this trend is predicted to continue. General PC products are the second-highest area of growth, with high-end gaming products only expected to have a small revenue uptick over the next few years. This reflects the appeal of AMD's high core-count EPYC processors, with impressive performance and comparatively affordable pricing. EPYC is used in large datacentres owned by Microsoft, Google, Amazon, and more. Google's largest cloud data centre uses EPYC 2, and the Archer2 supercomputer will use around 12,000 of these CPUs

The Bulldozer microarchitecture (and derivatives) used through most of the 2010s was leading AMD towards progressively worse results each year. This was despite having the exclusive contract to provide the APUs for both the Xbox One and Playstation 4 and having decent sales in the low-to-mid-range dGPU market. It is good to see AMD's position strengthening because of the carry-over effect that competition has on prices and generational improvements.

Source(s)